To

many observers, deflation was a thing of the past in the wake of the QE3. The Fed’s asset purchases, which drove down

bond yields to record lows, were thought to have tamed the global deflationary

problem once and for all. What they

didn’t count on was the floodtide of deflation breaking through the dikes and

barriers carefully constructed by the world’s central banks.

The

increasing deflationary pressure is most visible in Europe and Asia but will

soon wash up on U.S. shores in the near future.

A general deflationary trend is already visible in equity markets in

several major countries, a consequence of the final descent of the 120-year

Kress cycle. As that cycle approaches

its final bottom in late 2014 we can expect to see an increase in some of the

problems we’re just starting to see right now in the global economy.

One

of the most conspicuous victims of the deflationary Kress cycle is China. China has in fact led the recent malaise in

global markets starting with an 11% surge in short-term interest rates in

China. China’s overnight repo rate

increased by an incredible 25%. As

analyst Bert Dohmen commented, “China is extremely important for all business

leaders and investors….Because whatever happens to China will tremendously influence

the world economy and your investments.

Many large U.S. and European companies depend on China for a significant

portion of their sales and profits….A crisis in China will have global

repercussions.”

China’s Shanghai Composite Index has

been in a bear market since peaking in mid-2009. It’s remarkable when you consider that as the

rest of the world has experienced a measure of recovery for the last four

years, China’s stock market has been in decline. In fact the Shanghia index is on the verge of

testing its 2008 credit crisis lows, as you can see here.

One of the most fundamental pillars

of market analysis is that the stock market always predicts future business

conditions. What is this telling us

about China’s business and economic future?

The message can’t be interpreted as anything but negative for the

nations of the world that depend on China’s manufacturing sector.

Then there is Russia. Not that Russia is of any great importance to

the global economy by itself, but Russia has long been a benchmark for

deflationary pressures. Since much of

Russia’s economy is tied to oil and natural resources, any sustained decline in

the price of oil will automatically exert a negative impact on the country. Remember back in 1998 when oil prices

collapsed to $10/barrel? Russia’s

financial sector went into collapse and its economy was in shambles. It took an oil price recovery in the last

decade to allow Russia’s economy to bounce back and grow for nine straight

years. Without the artificial oil price

inflation, thanks in large part to the Fed and other central banks, Kress cycle

deflationary forces would have long since wiped out Russia.

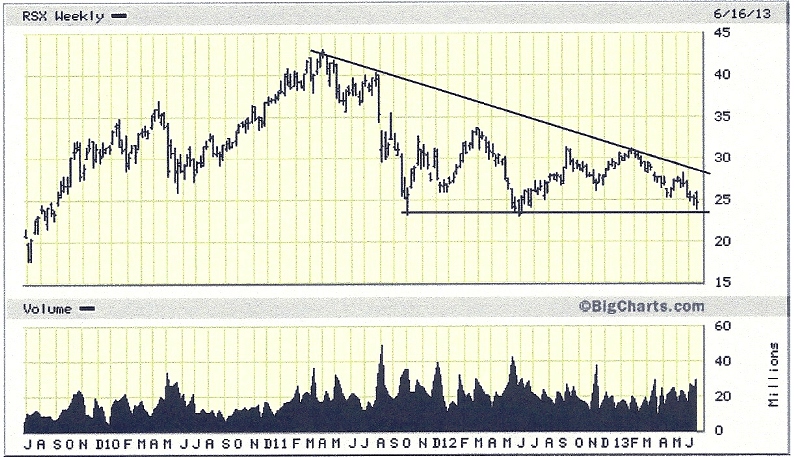

Here’s what the Market Vectors

Russia ETF (RSX) looks like over the last four years. Note the bear market pattern visible in this

chart since 2011. Any further decrease

in the price (and demand for) oil won’t bode well for Russia and will only

hasten the country’s economic demise.

What about the other BRIC

countries? India’s stock market is

currently probing a 4-year low and the country’s debt market had to be shut

recently as yields increased beyond trading bands. Brazil, which was the rising star of the

emerging markets not long ago, is slowing economically and has been described

recently as “dysfunctional.” Not

surprisingly, the natives are growing restless.

As Reuters reported on June 24, “More than a million Brazilians have taken to the

streets this past week in the largest mass demonstrations since the impeachment

of President Fernando Collor de Mello in 1992.”

Brazil’s stock market, as reflected in the MSCI

Brazil Capped Index Fund (EWZ), has broken down from a bearish triangle pattern

– a pattern much similar to the one visible in the Russia ETF shown above. This could be a preview of what’s to come for

other emerging markets in the not-too-distant future as we draw closer to the

120-year cycle bottom.

No comments:

Post a Comment