The

Federal Reserve guessing game ended Thursday after the FOMC made its decision

on interest rate policy. The Fed left

rates unchanged in a tip of the hat to investors who felt the economy was

vulnerable to overseas weakness. This

was what most on Wall Street wanted, although there was a sharp intraday

reversal after the announcement (apparently a case of buy the rumor, sell the

news).

In

last week’s commentary I emphasized that there was a built-in Wall of Worry for

stocks to climb based on the recent spike in bearish investor sentiment. There’s still a lot of short interest in the

market which could be used to fuel a short covering rally, especially now that

Fed interest rates are unchanged.

There’s no denying that equities love low interest rates, and the longer

the Fed leaves the benchmark rate unchanged the better it bodes for

investors. Whether or not it actually

helps the economy is a different story, however.

There

seems to be some contention among pundits as to whether the Fed should raise interest rates before the

year is over. The hawks maintain that

keeping rates near zero would only encourage another equity market bubble and

eventually lead to another credit crisis down the road. The doves insist that the longer the Fed

funds rate remains at or near zero, the more stimulative it will prove for the

financial market and the banking system.

My view is that bubbles occur when the Fed funds interest rate fails to

keep pace with Treasury yields. Considering

that government bond yields aren’t much higher now than they were at the depths

of the 2008 credit crash, I see no problem with keeping the Fed funds rate low

for a while longer. At the end of the

day, though, it’s up to investors to decide whether or not they like the Fed’s

policy.

Assuming

the market is ready to kick off a recovery rally, there are a couple of areas

in need of improvement. I’d like to see

some continued improvement in the market’s internal condition first and

foremost. The minimum requirement for

internal repair is a diminution of the NYSE new 52-week lows. On a positive note, the number of stocks

making new lows has diminished each day since Sept. 11. Moreover, we finally saw the first day since

Sept. 3 in which there were fewer than 40 new lows on Thursday, Sept. 17. If the new 52-week lows remain below 40 for

the next few sessions it will confirm that the market has returned to a normal,

healthier internal state.

The

NYSE Hi-Lo Momentum indicator series known as HILMO is based on the new 52-week

highs and lows and shows the stock market’s path of least resistance on a

short-, intermediate-, and longer-term basis.

The short-term directional components for HILMO are looking better than

they have in a long while but still need more improvement. You can see here that they’re trying to turn

up in sustained fashion, though. If it

continues from here it will support the bulls’ attempts at rallying the major

indices back to the pre-panic levels from early August.

Meanwhile,

the intermediate-term HILMO components are in even greater need of

reversal. Note the continued downward

trend reflected in the sub-dominant interim (blue line) and dominant interim

(red line) indicators shown below.

The

decline in the intermediate-term HILMO components shown above is consistent

with the fact that our intermediate-term trend indicator is still technically

bearish. To get a renewed

intermediate-term buy signal we need to see a majority of the six major indices

back above their 30-day and 60-day moving averages on a weekly closing basis.

Our

immediate-term (1-3 week) trend indicator has confirmed a bottom, however. All six of the major indices – the Dow, SPX,

NDX, NYA, MID and RUT – have all closed at least two days higher above their

15-day moving averages to confirm the bottom.

This technically paves the way for a relief rally. It’s worth mentioning that panic declines are

usually reversed within a couple of months once the fear that catalyzed the

sell-off has completely dissipated.

It’s

also worth mentioning that the Dow Jones Transportation Average (DJTA) has

erased most of its losses which it sustained during the “flash crash.” This has positive implications for the Dow

Industrials, shown above. Keep in mind

that the DJTA led the way lower for the Industrials heading into August. It’s constructive, from a Dow Theory

perspective, that the Transports are showing relative strength at this time.

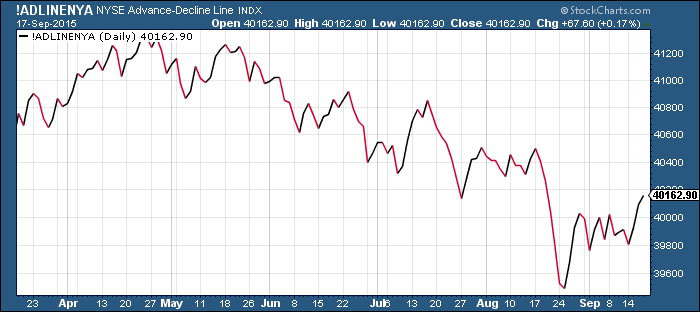

The

NYSE Composite Index (NYA), which I consider to be the most comprehensive

measure of the U.S. stock market, has barely budged higher recently and hasn’t

yet broke out of its 3-week consolidation pattern. By contrast, the NYSE advance-decline (A-D)

line is finally starting to show relative strength. One of the things I like to see at a market

bottom is for the A-D line to show leadership versus the NYA. This has started to happen, and if it

continues should bode well for the prospects of the NYSE Composite Index.

No comments:

Post a Comment