A

growing number of market technicians, some of them highly respected, are

forecasting a sharp correction in the January-February time frame. In light of a number of recent inquiries I’ve

had regarding this possibility, let’s examine this topic.

Tom

DeMark is one of Wall Street’s most esteemed technical analysts. He recently uncovered an analog between the

current stock market and the run-up to the 1929 top. Tom McClellan published a chart comparing the

two markets in a recent article. The theory behind price pattern analogs is

that “similar market conditions can produce similar patterns” as McClellan put

it.

One problem with comparing stock market

patterns from different periods is that the underlying conditions behind the

patterns are often dissimilar. For

instance, the run-up to the 1929 high was fueled by widespread speculation from

the general public. Today the public is

a virtual non-participant in the market’s run-up to new highs. Also, as McClellan himself points out, the

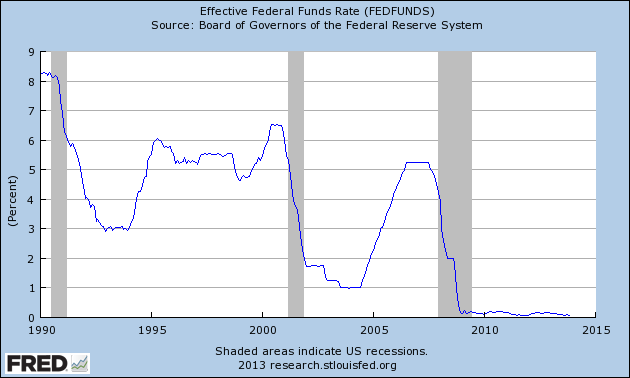

Federal Reserve consistently raised the benchmark interest rate several times

leading up to the 1929 crash. Today, of

course, the Fed funds rate is hovering near zero percent.

Technicians like DeMark and McClellan who foresee

a market top in mid-January base their prediction not just on various technical

disciplines, but on a more mundane set of reasons. For instance, next month is when the current

congressional agreement on the debt ceiling comes up again for discussion,

which in turn could cause investors to reassess their enthusiasm. Concerns over health insurance policies and

the implementation of the Affordable Care Act could be another investor concern

around mid-January. This is what the

technicians who argue in favor of a January top believe at any rate.

Another consideration for the projected

mid-January top is found in the following words of McClellan: “The Fed is not likely to yank away the

punchbowl at its Dec. 17-18, 2013 meeting, just a week before Christmas, but

the Jan. 28-29, 2014 meeting is a greater possibility for finding out that the

markets may have to start to quit the QE addiction. And the FOMC's March 18-19 meeting fits right

about where the Black Thursday crash of 1929 fits into this analog.”

My assessment of the mid-January top scenario is

decidedly different from that of the above mentioned technicians. There are several key short- and

intermediate-term cycle peaks scheduled for January, culminating with a Feb. 21

cycle cluster on the Kress cycle calendar.

This makes it possible a sharp correction beginning in January and

lasting into later February, but without a specific catalyst a crash is

exceedingly hard to predict.

Certainly the market's internal momentum is

deteriorating, but that alone isn’t sufficient to expect a major crash.

In order to have a sharp sell-off like the one DeMark, McClellan, et al

predict we'd likely need to see a major worry – probably news-related – take

center stage early next year.

Another consideration for a significant market

decline in 2014 is the “melt-up” scenario discussed by economist Ed Yardeni and

others. Should the stock market continue

its advance unabated into Q1 2014, conditions may well be ripe for a major top

by the end of the next quarter. The

weekly configuration of Kress cycles would support this, not to mention the

coming final “hard down” phase of the longer-term yearly cycles scheduled to

bottom in late 2014.

The only other ingredient necessary is greater

public participation in the stock market.

Michael Sincere of MarketWatch.com touched on this in a recent

column. He asks where are the

“intoxicated investors, a buying frenzy, over-the-top speculation, and a

get-rich-quick mentality?” He rightly

points out that these are necessary accompaniments to a market bubble.

A continued rally to new highs, however, will

likely solve this “problem” by forcing sidelined investors into becoming market

participants for fear of missing the proverbial “only game in town.” Thus as we’re about to enter 2014 the stage

may be set for a final melt-up stage to set up a crash later in the year.